Estate planning can seem like a very daunting task to many. After all, anything that is related to thinking about your death is quite overwhelming, and that includes deciding what you want to happen to all your assets.

Since the subject isn’t exactly fun to talk or think about, many stall planning their estate. In fact, according to the American Bar, over 55 percent of US citizens who die don’t have an estate plan or will in place. Similarly, approximately 71 percent of people haven’t updated their wills.

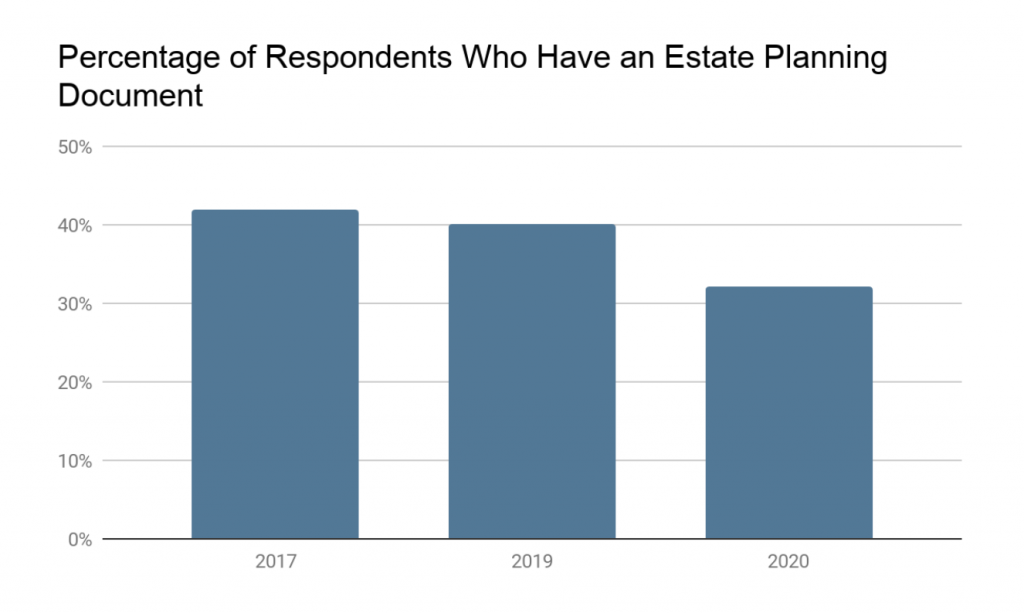

As depicted in the graph below, the number of people who respond to having a valid and updated estate planning document has decreased in the past three years!

Source

However, deciding what will happen to your assets and who will assume control of what is a decision you must make in your life to avoid confusion about inheritance as well as ensure that your heirs don’t overpay their taxes. That’s why professionals from sites like burzynskilaw.com are your allies.

To simplify the process, here are the top things you must do before planning your estate.

- Create an inventory of your assets

Begin by listing down all of your assets. After all, only once you know your current inventory of assets can you decide how to distribute it all.

Make sure to go through both tangible and intangible assets. The former will include items like vehicles, properties, electronics, jewelry, and collectibles. The latter can consist of IRAs, life insurance policies, bank accounts, brokerage account, stock shares, etc.

Apart from creating an inventory, also make sure to write down where all the physical documentation is and who is the point of contact for all non-physical possessions.

- List down your debts

Your assets aren’t the only thing that you must plan. You must also pass down any debt payments that you make. This can include auto loans, home equity lines, open credit cards, etc.

Create a separate list of all the debts you owe. Even if you don’t use a given credit card a lot, make sure to include it in the list as a list of items. If there are any physical documents associated with the debt, mention their location as well.

After you have completed the list of assets and debts, make a point of signing and dating it. Make multiple copies and given a copy each to your estate administrator and spouse. Also, store one in a safe deposit for emergencies and keep one copy handy with you.

- Name your beneficiaries

Once you have created a list of your assets, now is the time to decide how to distribute your estate among your beneficiaries. For this, you must first name your beneficiaries. Generally, this tends to include people’s blood family, including their spouse, siblings, and children.

However, others can choose to donate part of their assets to charity or funds. Regardless of what you decide, name every beneficiary. You can then proceed to register your stocks, bank accounts, and other intangible assets to be automatically transferred or “payable on death” to your assigned beneficiaries.

- Draft a proper will

Did you know that every individual over the age of 18 must have a will? This is imperative to protect your heirs and beneficiaries from loss. Therefore, once you are of age, draft a proper will.

All the planning you have done above will make drafting a will relatively easy. An estate planning attorney will take care of the legalities and loopholes of the document. Also, these documents aren’t expensive to create, so if you are solely avoiding it because of the burdening legal cost, rethink your decision.

Whenever you create your will, you must remember to date and sign it. Do so in front of two witnesses that are not related to you. Have it notarized. This will provide any fraud later on.

- Assign an executor

There are various people that will be involved in the estate planning process. Apart from your heirs, you must also decide who the executor will be. This individual will be a focal person for ensuring that things go as per your last wishes.

They will have to present your estate planning document in probate court as well as make sure that your property is distributed to your assigned beneficiaries.

Who should be your executor?

Well, you can choose anyone you can trust with the job. This includes your adult children, family friend, spouse, or an agent.

- Hire an estate planning attorney

As per the data collected by the Wealth Advisor, only 10 percent of people without wills or estate planning documents have actively sought the advice of attorneys. This is a very alarming statistic.

Whether you plan on finalizing your estate planning in the near future or not, an estate planning or will attorney is the best person to seek out. This is because only a professional can tell you the technicalities of the process as well as guide you about it all. So, do consult a professional from the get-go.

And once you have decided to plan your estate, hiring an attorney becomes a necessity. Here, it is better to hire a professional who practices within the same state. For instance, if you live in Plano, Texas, an estate planning attorney Plano has to offer will be well-versed in the state laws of Texas. In addition, if you need a living trust in California, a lawyer from law firms like CunninghamLegal should be able to help you.

- Review and update

Life is quite unpredictable and dynamic. Estate planning documents created a few years ago might become obsolete today.

To name a few life-changing events, your designated executioner or heirs might have passed away. You could have gotten a divorce or had another child. You might have gained or lost assets.

Therefore, you need to review your will every two years, at least. Update your will if need be.

Long Story Short: It has to be done!

As much as you hate the idea of organizing your assets and deciding on the various elements, procrastination won’t get you anywhere.

Yes, the thought of dying is very morbid. But leaving your loved ones unprotected is worse! So, plan your estate in a timely manner.